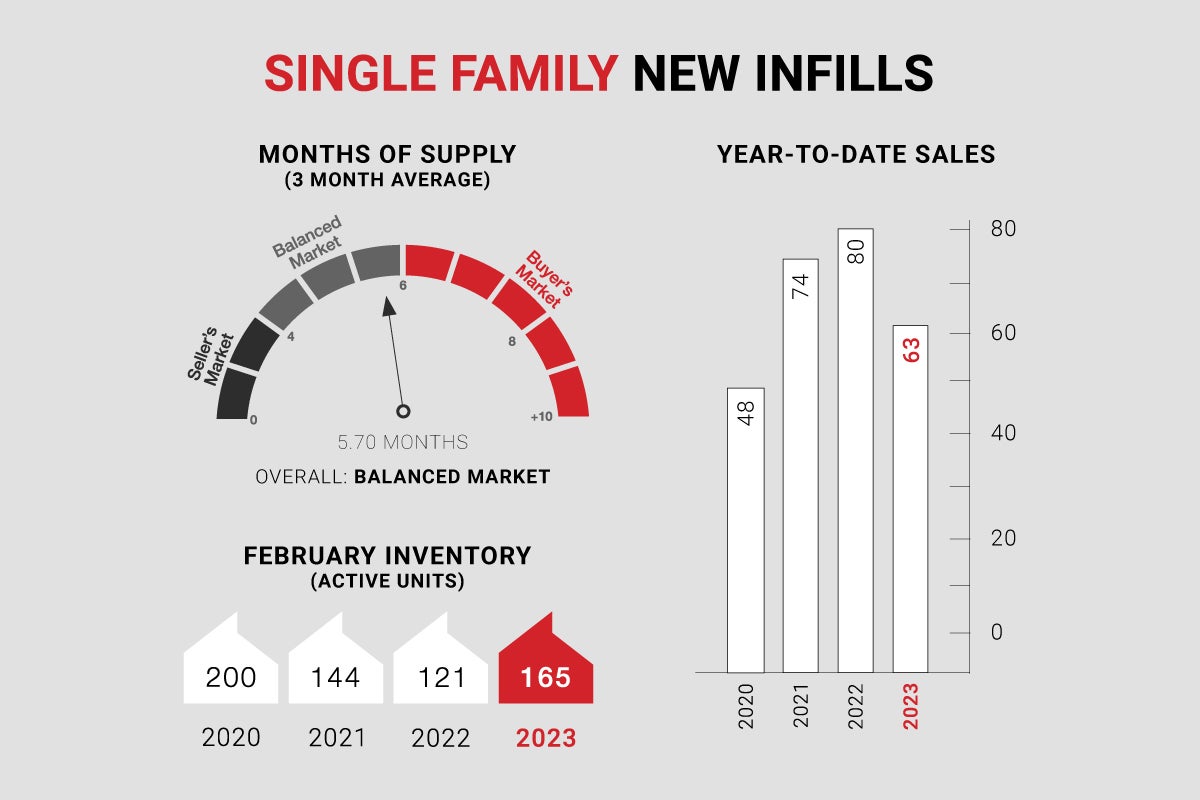

Single-family new infills posted 30 sales during the month of February, slightly down from the 33 sales recorded last month and down considerably from the 43 sales posted in February of last year.

Single-family new infill inventory increased further, to 165 active listings, from 141 active listings recorded last month, and is also higher than figures recorded at this time last year which was 121 active listings.

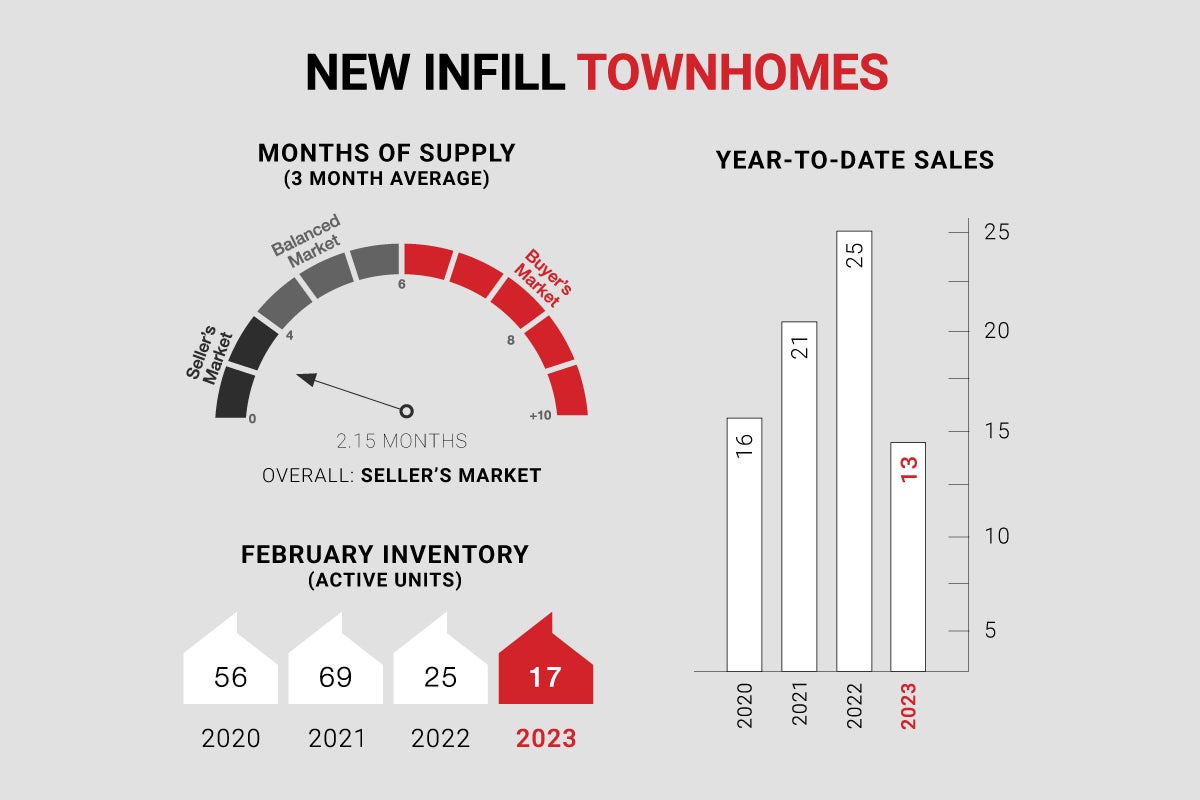

New infill townhomes posted 6 sales during the month of February, down from the 7 sales recorded in January and down considerably from the 15 sales recorded in February of last year.

New infill townhome inventory has increased, to 17 active units for sale, from 11 active units recorded last month and 25 active units recorded at this time last year. New infill townhome inventory remains well below long-term averages.

Although sales activity is lower than in previous years around this time, supply is the bigger constraint rather than affordability. As buyers wait patiently for new inventory to enter the market over the coming months, expectations will need to be managed carefully as supply will likely be inadequate to satisfy short-term pent-up demand, especially in the lower price points.

CALGARY MARKET UPDATE (CREB)

City of Calgary, March 1, 2023 - Consistent with typical seasonal behaviour sales, new listings, and inventory levels all trended up compared to last month. However, with 1,740 sales and 2,389 new listings, inventory levels improved only slightly over the last month and remained amongst the lowest February levels seen since 2006.

“While higher lending rates are impacting sales activity as expected, we are seeing a stronger pullback in new listings, keeping supply levels low and supporting some stronger-than-expected monthly price gains,” said CREB® Chief Economist Ann-Marie Lurie. “Prices are still below the May 2022 peak and it is still early in the year. However, if we do not see a shift in supply, we could see further upward pressure on prices over the near term.”

Both sales and new listings declined over last year’s record high for the month. While sales activity remained stronger than long-term trends and levels reported throughout the 2015 to 2020 period, new listings fell below long-term trends.

With a sales-to-new-listings ratio of 73 per cent and a months of supply of under two months, the market has struggled to move into balanced territory causing further upward pressure on home prices. The unadjusted benchmark price increased by nearly two per cent over January levels and last year’s prices.