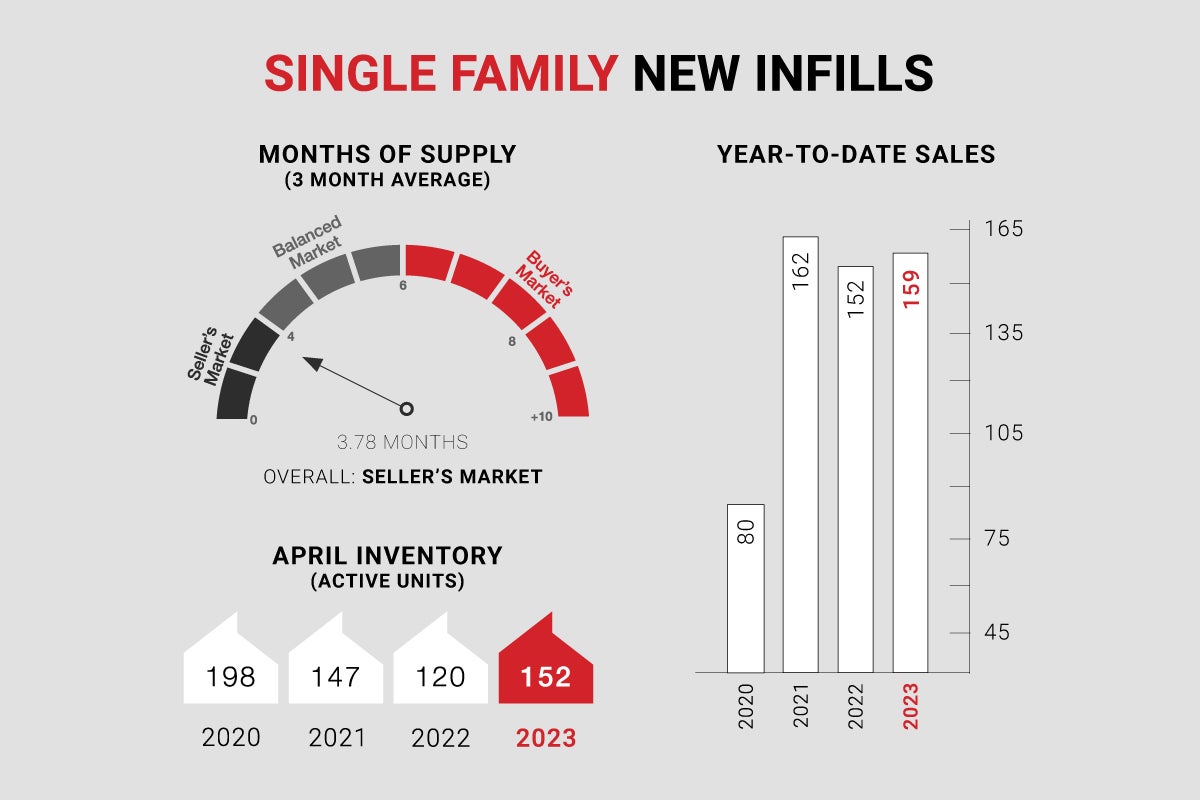

Single-family new infills posted 42 sales during the month of April, down from 54 sales recorded last month however up from 28 sales recorded in April of last year.

Single-family new infill inventory has eased, to 152 active listings, from 159 active listings recorded last month and is down from 120 active listings recorded at this time last year.

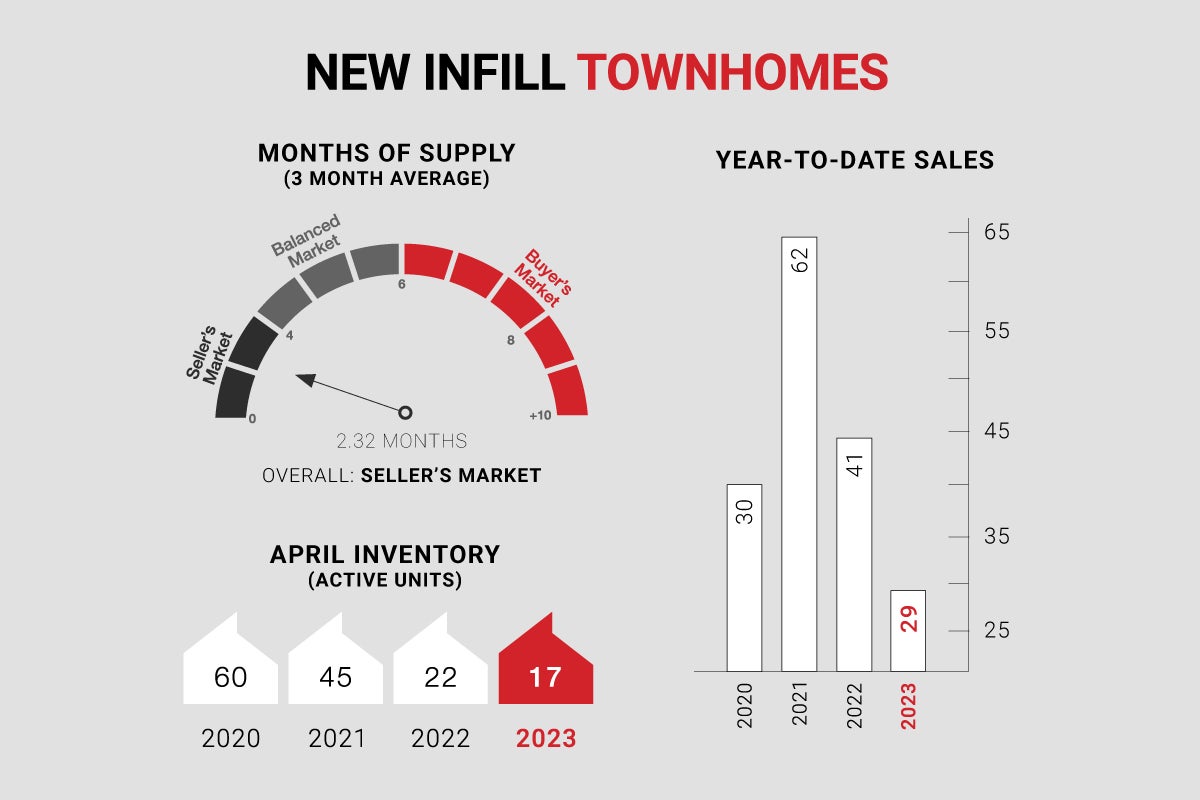

New infill townhomes posted 5 sales during the month of April, down from 11 sales recorded in March and down from 7 sales recorded in April of last year.

New infill townhome inventory has been unchanged since the beginning of February, with 17 active units for sale and is down from 22 active units recorded at this time last year.

With supply in the MLS market severely constrained, we expect upward pressure on prices in all segments. Although months of supply in the new infill sector might seem higher than the overall market, much of the inventory that is currently available is under construction, with minimal relief on the horizon.

CALGARY MARKET UPDATE (CREB)

City of Calgary, May 1, 2023 - Persistent sellers’ market conditions placed further upward pressure on home prices in April. After four months of persistent gains, the total unadjusted benchmark price reached $550,800, nearly two per cent higher than last month and a new monthly record high for the city.

“While sales activity is performing as expected, the steeper pullback in new listings has ensured that supply levels remain low,” said CREB® Chief Economist Ann-Marie Lurie. “The limited supply choice is causing more buyers to place offers above the list price, contributing to the stronger than expected gains in home prices.”

In April, sales reached 2,690 units compared to the 3,133 new listings. With a sales-to-new-listings ratio of 86 per cent, inventories declined by 34 per cent compared to last year and are over 45 per cent below long-term averages for April.

While sales have eased by 21 per cent compared to last year, the steep decline in supply has caused the months of supply to ease to just over one month. This reflects tighter market conditions than earlier in the year and compared to conditions reported last April.