Sales and inventory for both single-family new infills and new infill townhomes remain consistent.

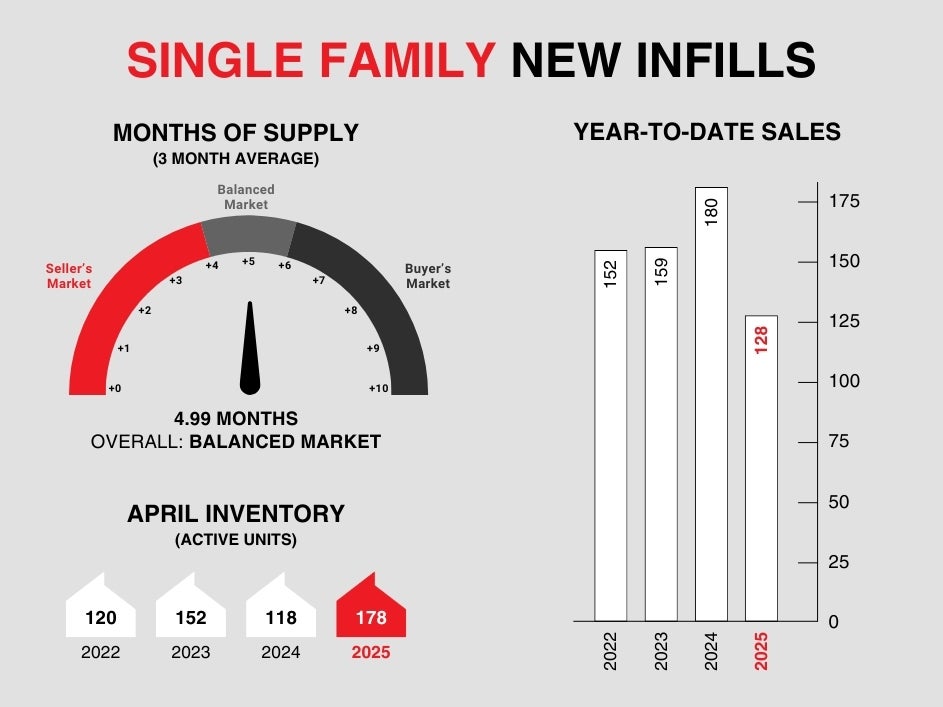

Single-family new infills posted 32 sales during the month of April, only slightly down from the 33 sales recorded last month, however considerably down from the 51 sales recorded in April of last year. Year-to-date sales for single-family new infills are sitting at 128 compared to 180 for the same period a year ago, down over 28%.

Single-family new infill inventory eased slightly, to 178 active listings, from the 185 active listings recorded last month however inventory is up over 50% compared to this time last year.

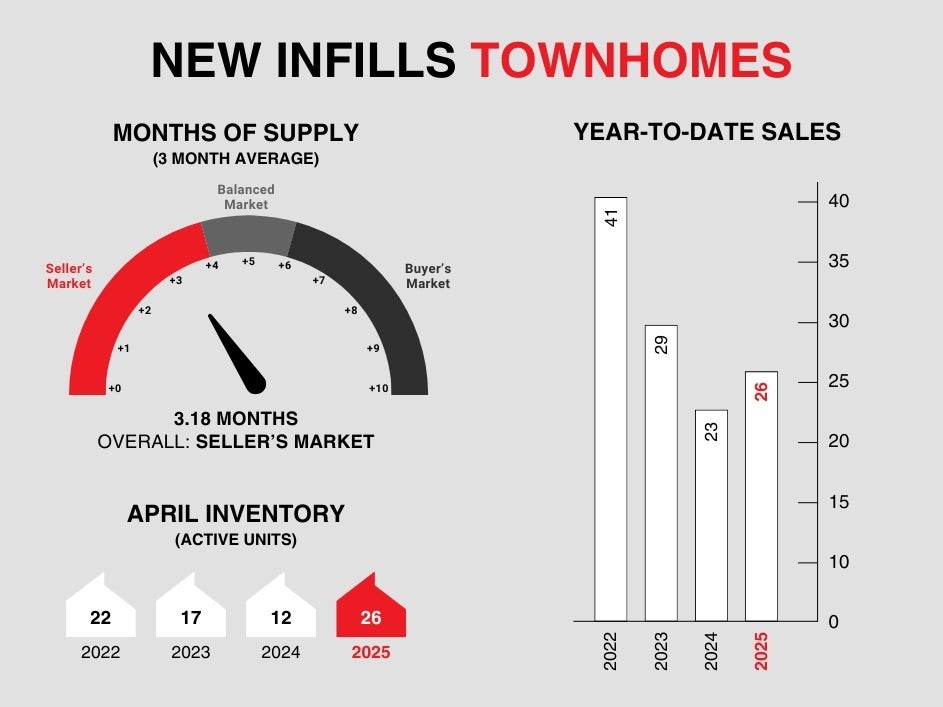

New infill townhomes posted 7 sales during the month of April, up slightly from the 6 sales recorded last month, and down slightly from the 9 sales recorded in April of last year. Year-to-date sales for new infill townhomes are 26 compared to 23 for the same period a year ago.

New infill townhome inventory is up slightly, to 26 active units for sale, from 25 active units recorded last month and is up considerably, from 12 active units listed for sale at this time last year.

As we approach the final weeks of the Spring market, new infill sales activity remains steady - however softer than what we experienced last year. Coming out of a market where inventory constraints held back overall sales, new inventory entering the marketplace over the past few months hasn’t been enough to push the needle by any substantial amount.

A boost in new listings this month relative to sales caused April inventories to rise to 5,876 units. Although this is more than double the number reported last year, last year’s supply was exceptionally low, and current inventory levels are consistent with what we typically see in April. April sales reached 2,236 units—22 per cent below last year’s levels but in line with long-term trends.

“Economic uncertainty has weighed on home sales in our market, but levels are still outpacing activity reported during the challenging economic climate experienced prior to the pandemic,” said Ann-Marie Lurie, Chief Economist at CREB®. “This, in part, is related to our market's situation before the recent shocks. Previous gains in migration, relatively stable employment levels, lower lending rates, and better supply choice compared to last year’s ultra-low levels have likely prevented a more significant pullback in sales and have kept home prices relatively stable.”

The rise in inventory levels helped the market shift to balanced conditions with nearly three months of supply. However, conditions vary depending on price range and property type. Lower-priced detached and semi-detached properties continue to struggle with insufficient supply, while row and apartment-style homes are seeing more broad-based shifts to balanced conditions.

The additional supply has helped relieve the pressure on home prices following the steep gains reported over the past several years. Benchmark prices for each property type have remained relatively stable compared to last month. However, compared to last year, detached and semi-detached prices are over two per cent higher than last year's levels, while apartment and row-style home prices have remained relatively unchanged.

Single-family new infills posted 32 sales during the month of April, only slightly down from the 33 sales recorded last month, however considerably down from the 51 sales recorded in April of last year. Year-to-date sales for single-family new infills are sitting at 128 compared to 180 for the same period a year ago, down over 28%.

Single-family new infill inventory eased slightly, to 178 active listings, from the 185 active listings recorded last month however inventory is up over 50% compared to this time last year.

New infill townhomes posted 7 sales during the month of April, up slightly from the 6 sales recorded last month, and down slightly from the 9 sales recorded in April of last year. Year-to-date sales for new infill townhomes are 26 compared to 23 for the same period a year ago.

New infill townhome inventory is up slightly, to 26 active units for sale, from 25 active units recorded last month and is up considerably, from 12 active units listed for sale at this time last year.

As we approach the final weeks of the Spring market, new infill sales activity remains steady - however softer than what we experienced last year. Coming out of a market where inventory constraints held back overall sales, new inventory entering the marketplace over the past few months hasn’t been enough to push the needle by any substantial amount.

Although high construction costs coupled with political uncertainty continues to weigh on new infill markets, Calgary remains a front runner compared to other cities throughout Canada in terms of overall affordability and opportunity.

CALGARY MARKET UPDATE (CREB)

City of Calgary, May 1, 2025 - Balanced conditions take pressure off prices

“Economic uncertainty has weighed on home sales in our market, but levels are still outpacing activity reported during the challenging economic climate experienced prior to the pandemic,” said Ann-Marie Lurie, Chief Economist at CREB®. “This, in part, is related to our market's situation before the recent shocks. Previous gains in migration, relatively stable employment levels, lower lending rates, and better supply choice compared to last year’s ultra-low levels have likely prevented a more significant pullback in sales and have kept home prices relatively stable.”

The rise in inventory levels helped the market shift to balanced conditions with nearly three months of supply. However, conditions vary depending on price range and property type. Lower-priced detached and semi-detached properties continue to struggle with insufficient supply, while row and apartment-style homes are seeing more broad-based shifts to balanced conditions.

The additional supply has helped relieve the pressure on home prices following the steep gains reported over the past several years. Benchmark prices for each property type have remained relatively stable compared to last month. However, compared to last year, detached and semi-detached prices are over two per cent higher than last year's levels, while apartment and row-style home prices have remained relatively unchanged.