Inventory in both single-family and townhome new infills inches upwards as sales hold steady throughout the summer months.

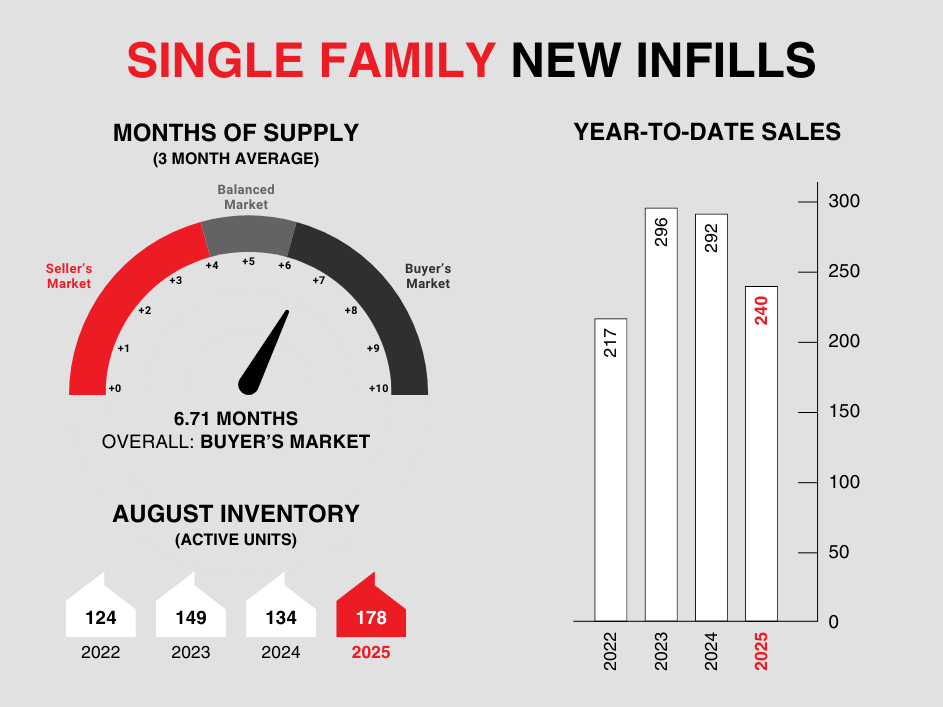

Single-family new infills posted 22 sales during the month of August, slightly up from 20 sales recorded last month and also up from 16 sales recorded in August of last year. That said, year-to-date sales for single-family new infills are down 17.8% compared to last year.

Single-family new infill inventory has also increased to 178 active listings for sale, compared to 160 active listings recorded last month, and 134 active listings recorded at this time last year.

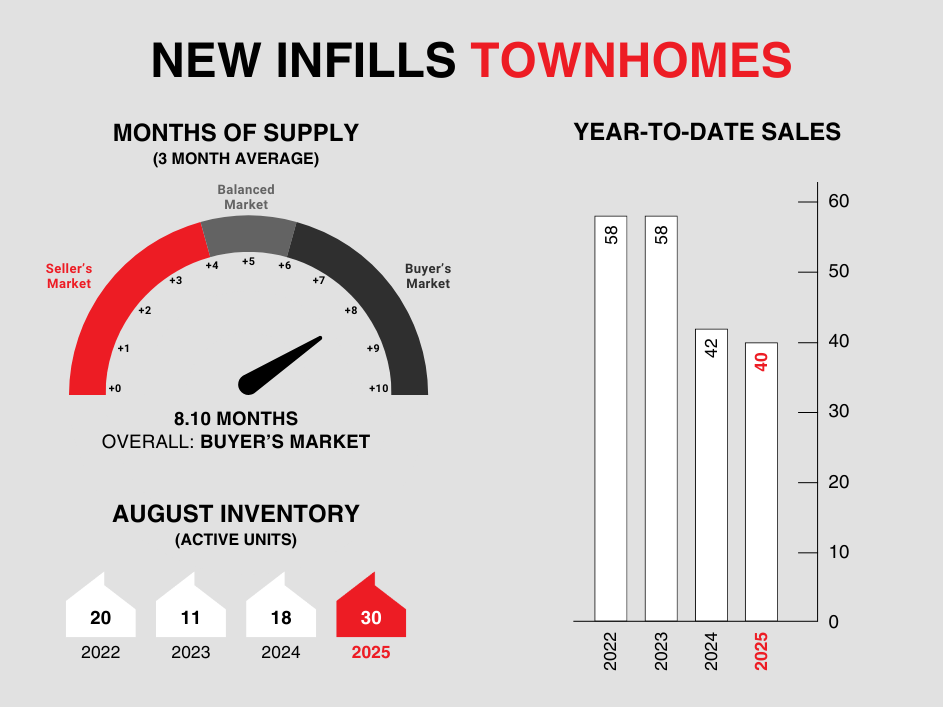

New infill townhomes posted 3 sales during the month of August, up from 2 sales recorded last month, however down from the 4 sales recorded at this time last year. Year-to-date sales for new townhomes are down 4.8% compared to the same period last year.

New infill townhome inventory is up to 30 active units for sale, an increase from the 27 active units for sale recorded last month and the 18 active units listed for sale at this time last year.

New infill sales activity is expected to continue its current pace while inventory levels continue to creep upwards. With market conditions starting to favour buyers, sellers will need to adjust pricing accordingly to be more competitive and secure sales in the short term.

CALGARY MARKET UPDATE (CREB)

City of Calgary, September 1, 2025 - Price declines mostly driven by higher density home types.

Improving supply choice has changed the dynamics of the Calgary market driving price declines over the past several months. Higher price adjustments are occurring for apartment and row style properties while detached and semi-detached properties have reported modest declines. As of August, the unadjusted total residential benchmark price was $577,200, down over last month and nearly four per cent lower than levels reported last year.

“Perspective is needed when it comes to price adjustments. The most significant price adjustments are occurring for row and apartment style homes as they are also the product type that are facing the largest gains in supply choice,” said Ann-Marie Lurie, Chief Economist at CREB®. “Meanwhile price adjustments in the detached and semi-detached markets range from modest price growth in some areas to larger price declines in areas with large supply growth. Overall, recent price adjustments have not offset all the gains that have occurred over the past several years.”

August reported 1,989 sales, nearly nine per cent lower than last year. Sales have slowed compared to the high levels reported over the past four years. However, activity is still above long-term trends, reflecting relatively strong demand. What has changed is the supply situation. New listings remain elevated, keeping the sales-to-new-listings ratio below 60 per cent and pushing inventory to 6,661, the highest August amount since 2019.

More inventory choice coupled with lower sales has caused the months of supply to rise to 3.4 months in August, much higher than the sellers' market conditions reported over the previous four years, but still well below the buyer market conditions observed prior to the pandemic. While the market is much more balanced compared to last year, there is significant variation depending on property type, price range and location.