Single-family new infill sales eased in 2025 while new infill townhome sales held steady.

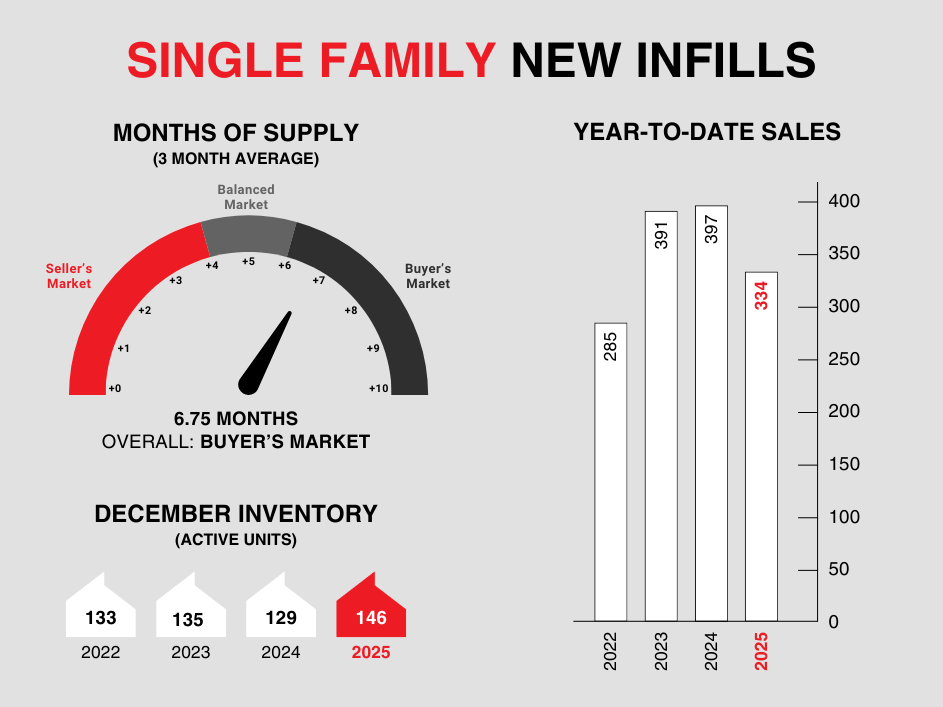

Single-family new infills posted 23 sales during the month of December, up slightly from 20 sales recorded in November, but nearly on par with the 24 sales recorded in December of last year. Despite a few strong sales months in 2025, total single family sales in 2025 came in at 334, down from the 397 sales posted in 2024, marking a 15.9% decline year over year.

Heading into 2026, single family new infill inventory has declined to 146 active listings, down substantially from the 206 active listings recorded at the end of November, but up 13% from the 129 active listings recorded at the beginning of 2025. Easing inventories through December are a fairly normal occurrence, as many unsold units are removed for a holiday break, or to be re-listed in the New Year. Many of these unsold properties are expected to return to the market in the coming weeks.

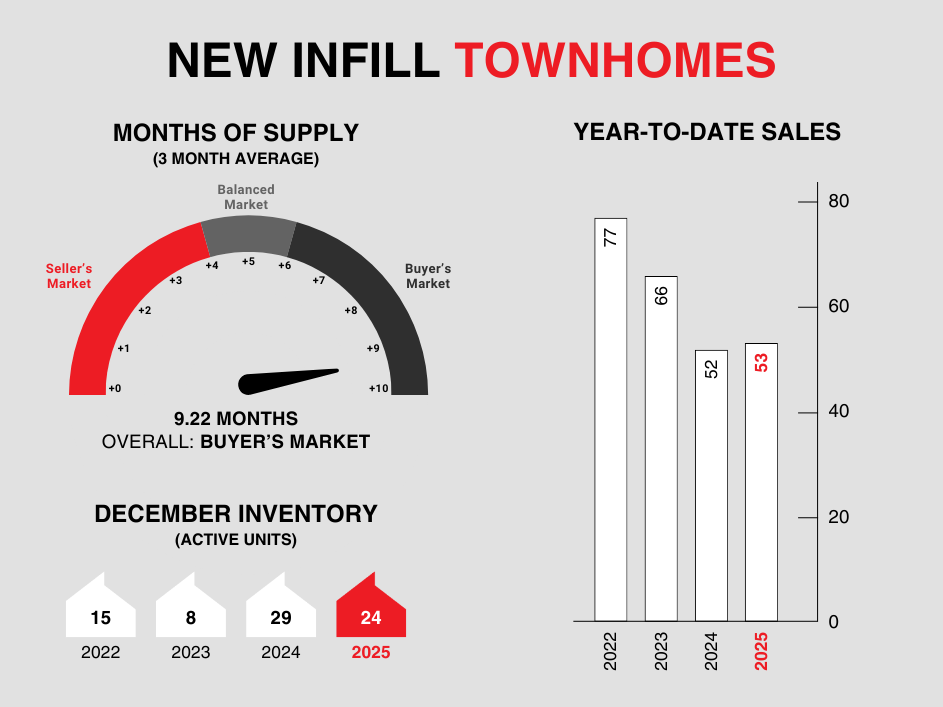

New infill townhomes posted 3 sales during the month of December, the same as the 3 sales recorded last month; however, it is still an improvement from no sales recorded in December of last year. Year over year, townhome sales in 2025 were nearly on par with 2024 sales, with 53 sales in 2025 compared to 52 sales in 2024.

Heading into 2026, new infill townhome inventory has declined to 24 active units for sale, from the 30 active units recorded at the end of November. This is also down slightly from the 29 active units listed for sale at this time last year.

Now that we are officially out of the holiday season and heading into 2026, sales activity and inventory levels are expected to increase as we slowly start to move towards the Spring selling season.

From all of us at the URBAN UPGRADE & NEWINFILLS team, Happy New Year!

CALGARY MARKET UPDATE (CREB)

Calgary, Alberta, Jan. 2, 2026 – Following several years of strong price growth, 2025 marked a year of transition thanks to strong demand and limited supply. Due to record-high starts, supply levels improved across all aspects of the housing market, just as demand pressure eased due to a reduction in migration levels and heightened uncertainty that persisted throughout the spring market. This helped shift the resale market from one that favoured the seller to one that was more balanced.

In 2025, sales reached 22,751 units, down 16% over last year, but in-line with long-term trends. Much of the shift came from the growth in supply. 2025 saw over 40,000 new listings come onto the market, 9% higher than last year, causing inventories to rise and driving more balanced conditions.

“Supply levels were expected to rise in 2025. However, the growth was higher than expected especially for apartment condominium and row homes. This weighed on prices in those sectors enough to offset the annual gains reported for both detached and semi-detached homes,” said Ann-Marie Lurie, CREB®’s Chief Economist. "Adjustments in both supply and demand varied across the city, with pockets of the market continuing to experience seller’s market conditions versus some areas where the conditions favoured the buyer. This resulted in different price trends based on location, price range and property type.”

Overall, the annual average total residential benchmark price in 2025 was $577,492, 2% lower than last year’s annual average. However, annual detached and semi-detached prices rose by a respective 1% and 3%, while apartment and row homes saw prices fall by a respective 3% and 2%.

Compared to other districts, the North East reported the largest decline in prices this year. While some of this is related to improved supply across all areas of the city, it is also important to note that the North East district also reported the strongest price growth over the past two years.

For the first time in three years, we are heading into the New Year with better inventory levels. Details on what is expected to happen in the market in 2026 will be released at CREB®’s annual Forecast Conference on Jan. 20, 2026.