New infill inventory and sales remain steady through the first month of the year.

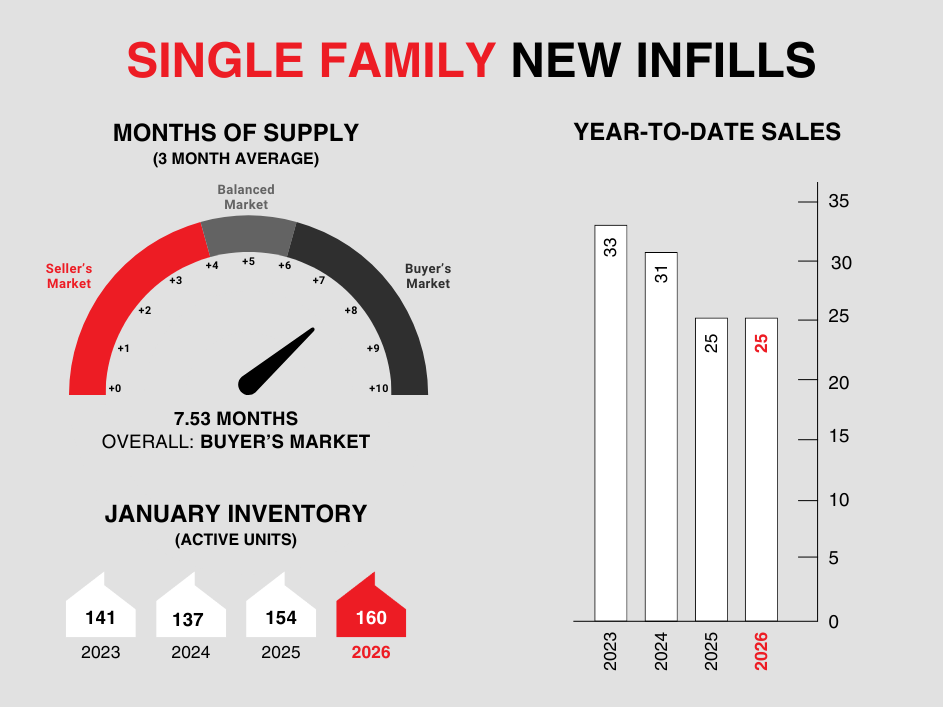

Single-family new infills posted 25 sales during the month of January, up slightly from the 23 sales recorded last month and on par with the 25 sales recorded in January of last year.

As expected, single-family new infill inventory has increased, up to 160 active listings from 146 active listings recorded last month. This is also up from the 154 active listings recorded at this time last year.

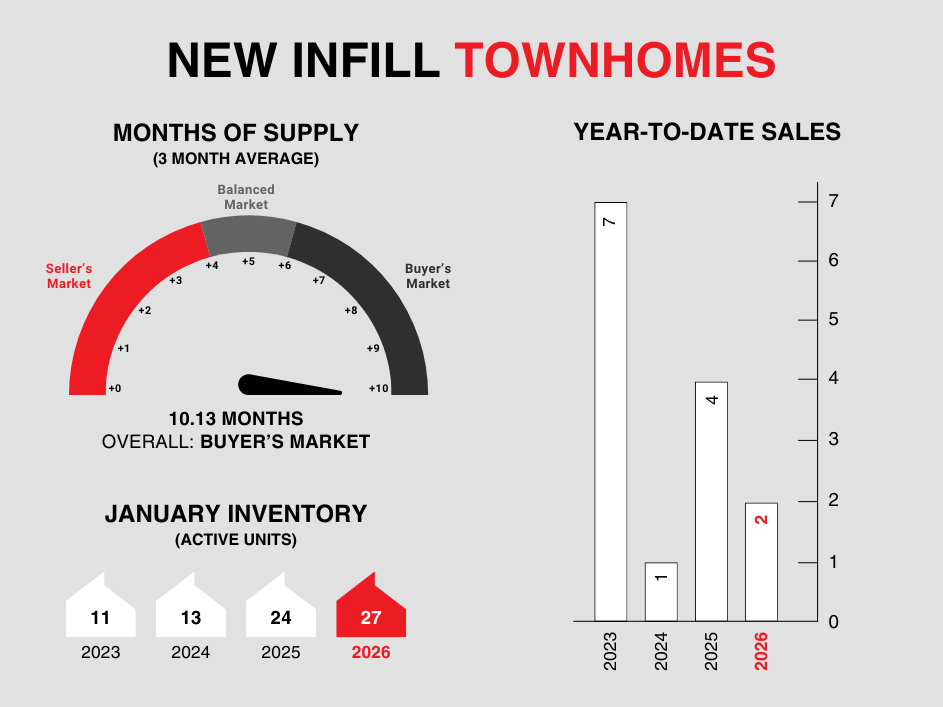

New infill townhomes posted 2 sales during the month of January, a slight increase from the 3 sales recorded last month, however down from the 4 sales recorded in January of last year.

New infill townhome inventory increased slightly through January, up to 27 active units for sale from 24 active units recorded last month. This is also up slightly from the 24 active units listed for sale at this time last year.

Although interest rates remain unchanged, we expect a healthy Spring market in the New Infill sector as demand remains quite stable for new homes in the inner city.

CALGARY MARKET UPDATE (CREB)

Calgary, Alberta, Feb. 2, 2026 – Calgary reported 1,234 sales in January, a year-over-year decline of 15 per cent, but in line with typical levels of activity for the month. While sales declined across all property types, the steepest declines occurred in higher-density homes.

“Following the typical December slowdown, potential buyers for high-density homes were more hesitant to return to the market in January, as increased supply choice across all aspects of the market has reduced the sense of urgency,” said Ann-Marie Lurie, CREB®’s Chief Economist. “At the same time, sellers were quick to bring their listings onto the market, causing the sales-to-new-listings ratio to drop to 44 per cent, mostly due to shifts in apartment and row-style homes. Overall, this is not entirely uncommon for January, as both buyers and sellers weigh their options ahead of the spring market.”

The rise in new listings compared to sales caused inventory levels to increase to 4,391 units, the highest January level since 2020. However, as with sales, conditions vary by property type, with row and apartment homes facing higher levels of inventory compared to long-term trends. The result is months of supply that ranges from under three months in the detached sector to five months for apartment-style homes.

Due to declines in the later part of 2025, benchmark prices are lower than levels reported at the start of last year. However, seasonally adjusted figures point to stable levels in January compared to the end of 2025. Nonetheless, year-over-year total residential benchmark prices have declined by nearly five per cent, as steep declines reported in the oversupplied row- and apartment-style homes weighed on total residential prices compared to last year.