The Calgary Real Estate Board (CREB) recently released their annual market and economic review and forecast. This annual report examines the housing sector, the local Calgary economy, and other variables that impact real estate, such as lending rates and migration patterns.

Here is a look at what CREB says about the Calgary economy. If you are looking for insights into the Calgary real estate market, visit our sister post: CREB 2025 ECONOMIC REVIEW & 2026 FORECAST

2026 Forecast Summary

FORECAST RISKS

Balanced Market Conditions

In 2025, housing market activity in Calgary shifted from favouring sellers to more balanced conditions as supply in the new-home, rental, and resale markets improved, coinciding with demand returning to more typical levels, largely due to slower migration levels. This took much of the pressure off home prices, especially in the apartment and row segments, which reported the largest gains in supply compared to long-term trends.

Elevated supply across new, resale, and rental markets, combined with stable demand, is expected to prolong the time required to absorb the additional resale supply currently in the market. Overall, balanced to buyer’s market conditions are expected to persist in 2026, depending on the property type.

Economic Risks

The recent MOU on new pipeline development and regulatory policy changes, signed by the provincial and federal governments, offers significant upside for our city and province if progress is made. However, the economic benefits are not expected to affect the housing market this year.

UPSIDE RISK TO THE FORECAST

Potential Increase in Investment Activity and Economic Confidence

Shifting stance with the federal government regarding regulatory barriers that impact the energy sector could support stronger-than-expected investment activity and improved confidence regarding our economic prospects.

DOWNSIDE RISK TO THE FORECAST

Uncertainty from US Tariffs and International Affairs

US tariffs and renegotiation of the Cusma Agreement will continue to create uncertainty, potentially causing some downside risk to economic conditions in 2026.

Key Economic Indicators

ECONOMIC SUMMARY

Alberta is expected to remain a national growth leader in 2026, supported by diversified investment and our energy sector. The economy fared better than most expected in 2025, but conditions have varied across the country as some provinces were harder hit by U.S. trade policies. Resource-rich economies like Alberta and Saskatchewan have been leading the country in growth, a trend that is expected to continue over the next two years. While significant upside potential exists for the province given recent pullbacks of regulatory policies, the benefit from rising energy investment activity is not expected to occur in 2026, especially given the weaker energy price environment. In the meantime, we continue to benefit from investment in petrochemicals, hydrogen, food processing, tech, critical minerals and aviation. While relative affordability is still a benefit for our province, migration is expected to slow in Calgary as unemployment rates remain elevated. With inflation returning to target levels, the Bank of Canada is likely done cutting rates in 2026, but previous increases in cost of living will continue to weigh on consumers.

EMPLOYMENT

Slower job growth in 2026 is expected to temper housing demand. Employment growth in the city exceeded expectations in 2025 with growth averaging four per cent. While notable job losses occurred in some segments of the market, most of the job losses occurred in the accommodation and food services sector, followed by manufacturing, business and other services. Meanwhile, most of the growth occurred in the healthcare and social assistance sector. While gains in this sector, along with real estate, retail and government, were expected thanks to the rising population, gains in professional-type jobs exceeded expectations for the year.

Unemployment rates remained high in Calgary as the growth in labour force, due to recent population gains, outpaced the number of jobs created. Employment growth is expected to slow in 2026 as job losses in public administration and manufacturing offset the gains expected in other sectors. While the size of our labour force is not expected to rise in 2026 as migration slows, the weaker employment growth is expected to keep unemployment rates at elevated levels. Previous employment gains will support typical levels of housing demand in 2026, but limited employment gains are expected to prevent any further growth in sales.

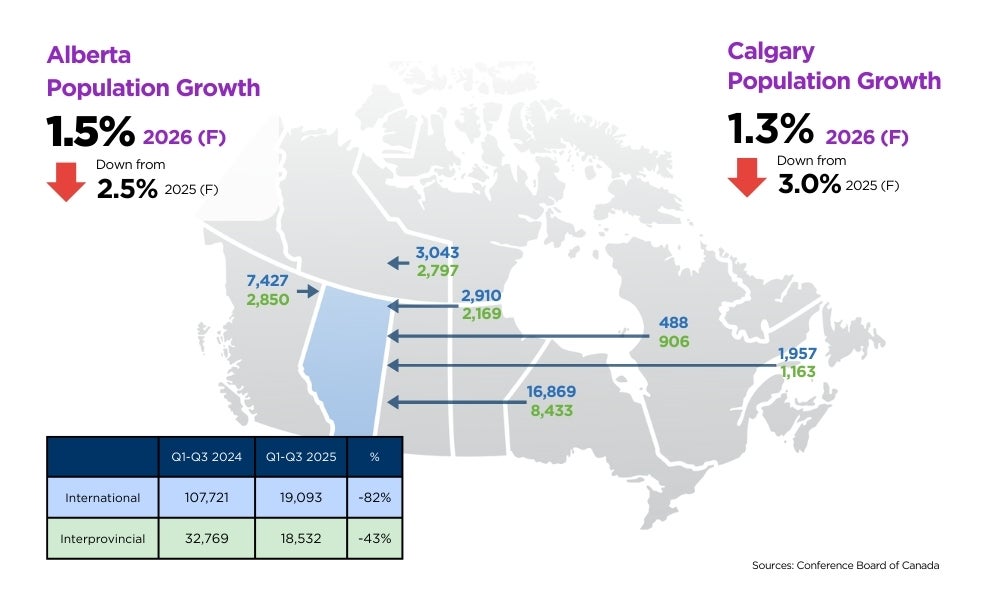

POPULATION

With migration returning to lower levels, sales are expected to remain in line with long-term trends. Strong population growth from 2022 to 2024 contributed to much of the supply challenges in the housing market. Estimates from 2025 point to a higher than expected reduction in the number of migrants coming to the province. As we move into 2026, migration levels are expected to ease further as more temporary migrants leave and fewer international migrants are allowed into Canada. Interprovincial figures are also expected to slow given weak employment gains in Calgary and elevated unemployment rates. Lower levels of migration are coming at a time when supply is rising, which ultimately will weigh on the local housing market in 2026. While migration is expected to slow, this is not the same scenario as what was experienced prior to the pandemic where, on an interprovincial basis, more people left Alberta than moved here. Nonethless, the current shift in conditions is expected to slow the demand for housing to levels more consistent with long-term trends.

HOUSING SUPPLY

NEW HOME

After years of record activity, new home starts are expected to ease in 2026 as migration slows and supply pressures emerge. New home starts exceeded expectations in 2025, with levels nearing another record high. As of November, starts were 26,439, surpassing 2024’s annual total of 24,369. Starts have been elevated since 2022 as the new home sector responded to the shortage of supply caused by a sudden increase in migration levels. However, with the number of migrants entering Calgary slowing and segments of the market showing signs of excess supply, we should start to see a pullback on new home starts in 2026.

New home construction is expected to slow in 2026, but elevated supply, particularly in the apartment sector, will continue to weigh on prices. While starts are expected to ease, there are still over 26,000 units under construction. Although 45 per cent of the units under construction are rental, new home supply levels should continue to rise as units are completed. Much of the additional supply is expected to occur in the apartment-style segment. This will have a significant impact on rental vacancies and rental rates, as 63 per cent of the 17,771 units under construction are rental. This additional rental supply will still impact the ownership market due to a slower transition from rental to ownership and a reduction in investor demand. The areas of the city with a larger share of units under construction are expected to weigh more heavily on resale pricing.

RENTAL

The scale of rental supply coming to the market relative to migration suggests vacancy rates will remain elevated through 2026. Purpose-built rental construction has been on the rise, reaching record levels following previous rental rate gains and low vacancies. However, the sudden pullback in international migration has come at a time when these units are becoming available in the market. This is driving higher vacancy rates and placing downward pressure on asking rents. There are still over 11,801 purpose-built rental units under construction, which will be completed over the next several years. With international migration numbers expected to remain at lower levels, it will take longer for the additional supply to be absorbed. This will likely keep vacancy rates elevated in 2026, further weighing on rental rates.