New infills post a strong month of sales activity as we head into the Spring selling season.

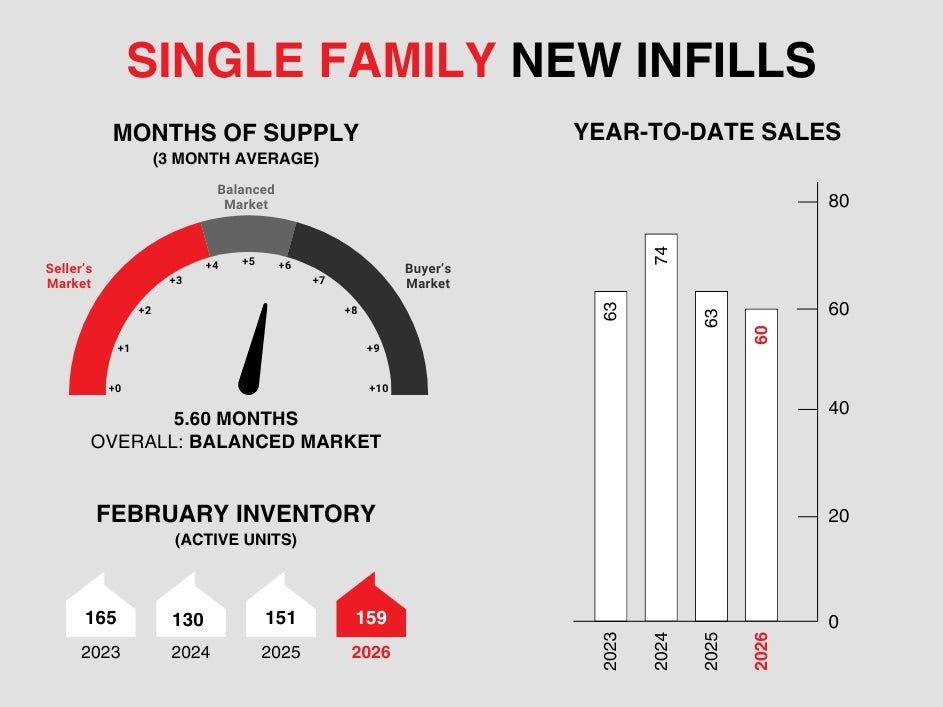

Single-family new infills posted 35 sales during the month of February, up significantly from the 25 sales recorded last month but slightly below the 38 sales recorded in February of last year.

Single-family new infill inventory has decreased slightly, down to 159 active listings for sale from the 160 active listings recorded last month, but up from the 151 active listings recorded at this time last year.

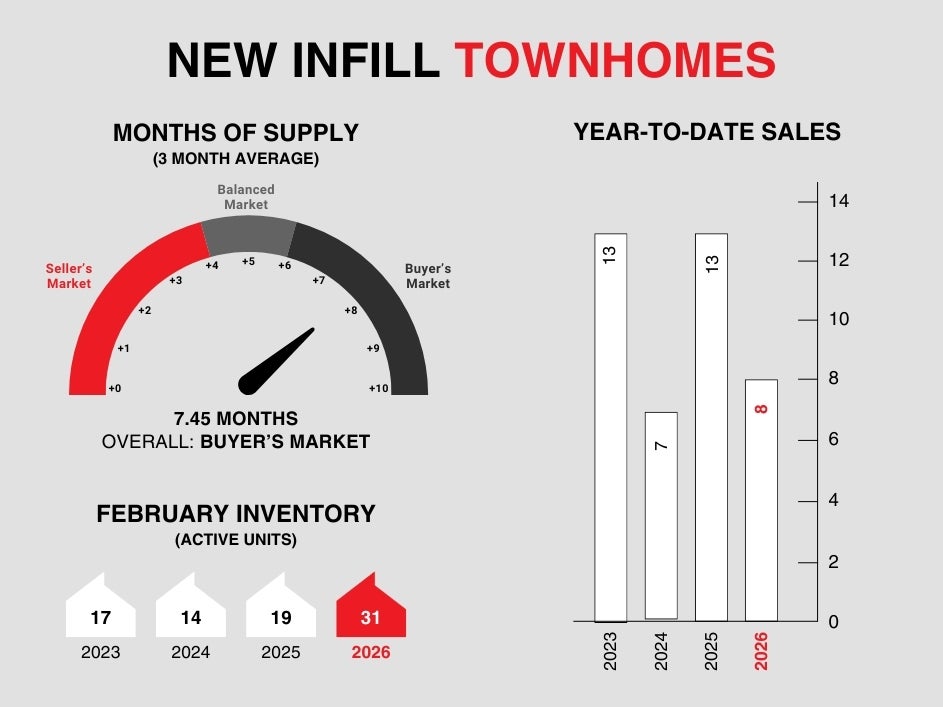

New infill townhomes posted 6 sales during the month of February, up significantly from the 2 sales recorded last month, however, down from the 9 sales recorded in February of last year.

New infill townhome inventory increased slightly, up to 31 active units for sale from the 27 active units recorded last month. This is also up significantly from the 19 active units listed for sale at this time last year.

Although the general Calgary market is softening compared to years past, the new infill market is holding steady. Demand remains especially high for quality inventory in premium locations, especially in the estate single-family sector.

CALGARY MARKET UPDATE (CREB)

Calgary, Alberta, March 2, 2026 – Calgary continued to see market conditions vary by property type in February. The tightest conditions occurred in detached and semi-detached properties, reporting less than three months of supply. Row homes reported slightly higher supply levels relative to demand but remained relatively balanced. Meanwhile, apartment-style properties are dealing with excess supply, as conditions continue to favour the buyer.

“Slowing migration levels are coming at a time when supply for apartment-style homes is rising. Calgary reported record high starts last year, mostly due to gains in apartment starts, where there are nearly 18,000 units currently under construction. While a large share of the units is targeted for rental, this also impacts condo ownership markets,” said Ann-Marie Lurie, CREB®’s Chief Economist. “Meanwhile, on the opposite end of the spectrum, the detached market remains relatively balanced in the higher price ranges and continues to struggle with limited supply for homes priced below $700,000.”

Tighter conditions for detached homes offset the higher supply levels in the apartment condominium sector, leaving citywide conditions relatively balanced at three months of supply and a sales-to-new-listings ratio of 55%. Inventory levels reached 4,822 units in February, with condominiums and row homes representing more than half of all the inventory. At the same time, there were 1,526 sales in February, an 11% decline over last February, mostly due to a sharp pullback in row and apartment sales.

Typical seasonal patterns tend to drive monthly gains in prices early in the year following the monthly slides reported at the end of the previous year. While February did report monthly benchmark price gains for most property types, prices continued to slide for apartment-style homes. However, monthly gains for lower-density homes offset the pullbacks for apartment units, leaving the total residential benchmark price of $560,500, 1% higher than January, but still 4% lower than last year's levels.