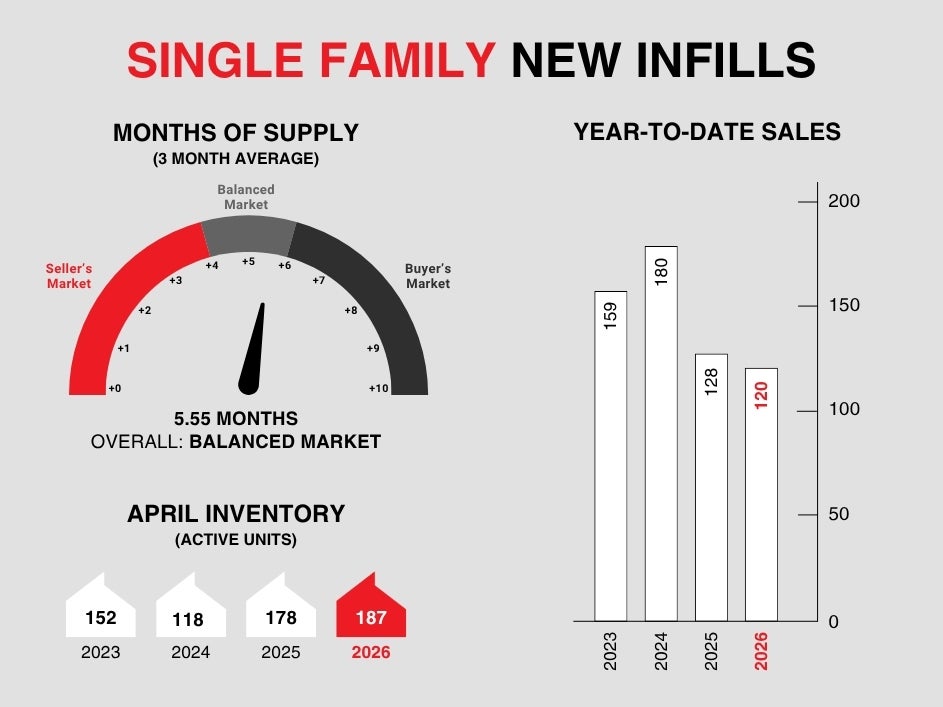

Single-family new infills post impressive sales in April, while new infill townhome sales ease.

Single-family new infills posted 35 sales in April, up considerably from the 25 recorded last month and up from the 32 recorded in April of last year.

Single-family new-infill inventory has increased moderately to 187 active listings for sale, up from 181 last month and up from 178 at this time last year.

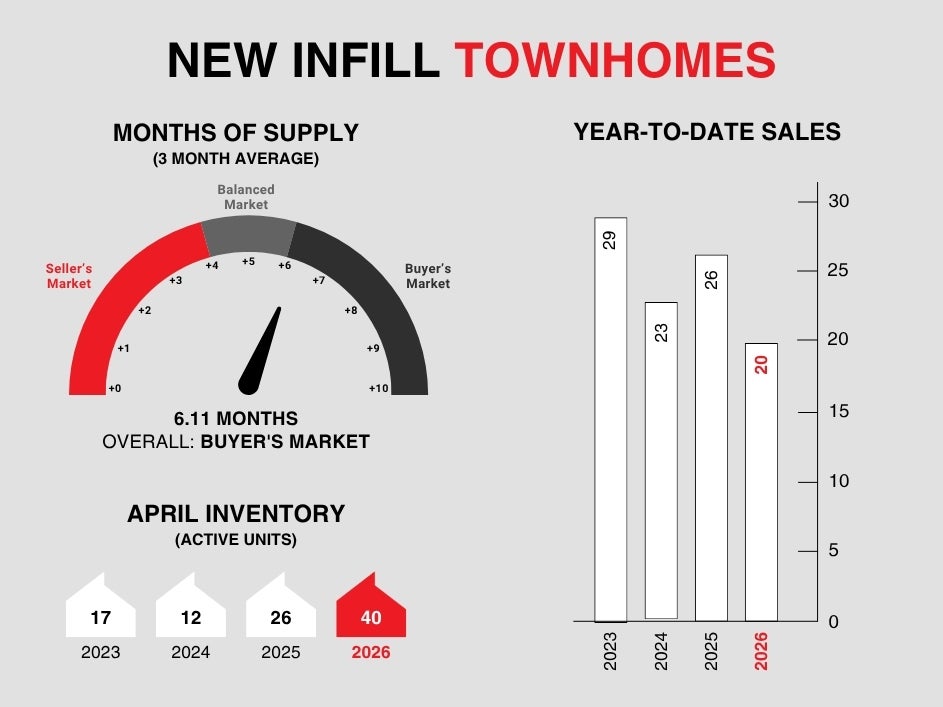

New infill townhomes posted only 3 sales in April, down from 9 last month and 7 in April of last year.

New infill townhome inventory increased further, to 40 active units for sale, from 39 active units recorded last month, and is up considerably from the 26 active units listed for sale at this time last year.

Now that Spring is finally here, the market seems to be waking up. Single-family new-infill sales are the strongest we’ve seen in many years, with a good portion at higher price points. Inventory is also at comfortable levels, giving buyers with means a healthy degree of choice.

CALGARY MARKET UPDATE (CREB)

Calgary, Alberta, May 1, 2026 – In line with seasonal expectations, both sales and inventory levels trended up relative to March’s activity. Despite this typical monthly rise, April sales totalled 2,104 units, 6% lower than levels reported in 2025.

“Sales were expected to ease this year as our market transitioned away from strong demand that was driven by previously rapid migration growth. Improved supply choice across the entire housing spectrum has reduced the urgency among potential purchasers, helping our market shift away from seller’s market conditions to more balanced conditions,” said Ann-Marie Lurie, CREB®’s Chief Economist. “However, the trend of limited supply choice in the detached market continues, while conditions favour the buyer in the apartment condominium market.”

With 3,829 new listings in April, the sales-to-new-listings ratio remained at 55%, supporting a modest monthly gain in supply. Inventory levels reached 5,973 units, nearly 2% higher than levels reported last April. Overall, the months of supply remained just below three, representing relatively balanced conditions. However, this ranged from just over two months for detached homes to over four months for apartment-style homes.

The unadjusted total residential benchmark price trended up compared with March, reaching $568,800. The monthly gain was mostly associated with seasonal improvements, which is expected heading into the spring market. Monthly gains were higher in the detached and semi-detached segments. Overall, compared with the previous year, prices remain 3% lower, with modest year-over-year declines in the detached and semi-detached sector, while declines neared 9% for apartment-style units.

So far in 2026, conditions have varied, ranging from seller’s market conditions and price growth for detached homes in some parts of the city to buyer’s market conditions and price adjustments in the apartment condominium sector.